The Financing Process

Demystifying Home Loans

The home loan process can feel overwhelming

By collaborating with a trusted lender and remaining informed through every step of the process, from pre-approval to closing, you can have a significantly more comfortable experience. You’ll want to consult with a mortgage specialist (or two) to find a professional who you are confident will provide you with the best care. To get an idea of what to expect, review the following home loan process steps.

VA Loans and Home Financing in San Diego: Frequently Asked Questions

I am Jose Luis Tepox Jr., a Military and VA Realtor serving Oceanside and North County San Diego. I am a Marine Corps veteran, and I help military and veteran families finance, buy, and relocate, including out-of-state PCS moves and VA loan purchases. Hablo Espanol.

What is a VA loan and who qualifies?

A VA loan is a mortgage backed by the Department of Veterans Affairs for eligible veterans, active-duty service members, and certain surviving spouses. Eligibility is based on your service history and a Certificate of Eligibility. I help you confirm yours and connect you with a VA-savvy lender.

Can I really buy with zero down and no PMI?

Yes. The VA loan allows eligible buyers to purchase with no down payment and no monthly private mortgage insurance, which lowers your monthly cost compared to most conventional loans. In high-cost San Diego, that benefit makes a real difference in what you can afford.

What is the VA funding fee, and who is exempt?

The funding fee is a one-time cost that helps keep the program running, and it can be rolled into the loan. Veterans with a service-connected disability rating are exempt from the funding fee, which lowers your total cost. I make sure you know exactly where you stand before you commit.

How does my VA entitlement affect how much I can borrow?

Your entitlement determines how much the VA will back without a down payment. If you have used your benefit before or carry a prior VA loan, your remaining entitlement still matters. I help you map your real buying power before we start the search.

Can I use a VA loan more than once?

Yes. The VA benefit is reusable, and in some cases you can have more than one VA loan at a time or restore entitlement after a sale or refinance. This matters a lot for service members who PCS and need to buy again at a new duty station.

What closing costs should a VA buyer plan for?

Expect lender fees, title and escrow, and the funding fee if it applies. In many cases we negotiate seller credits to offset costs. I give you a clear estimate up front so there are no surprises at the table.

How do I reach you to get started?

Call or text me direct at (619) 485-8293, email luis@joseluistepoxjr.com, or book a 15-minute call at calendar.app.google/RzYSyirMa3hKgPk2A. Tell me your timeline and whether you are using a VA loan, and I will map out the next steps.

Jose Luis Tepox Jr. | Military & VA Realtor | PAK Home Realty | DRE #02229757

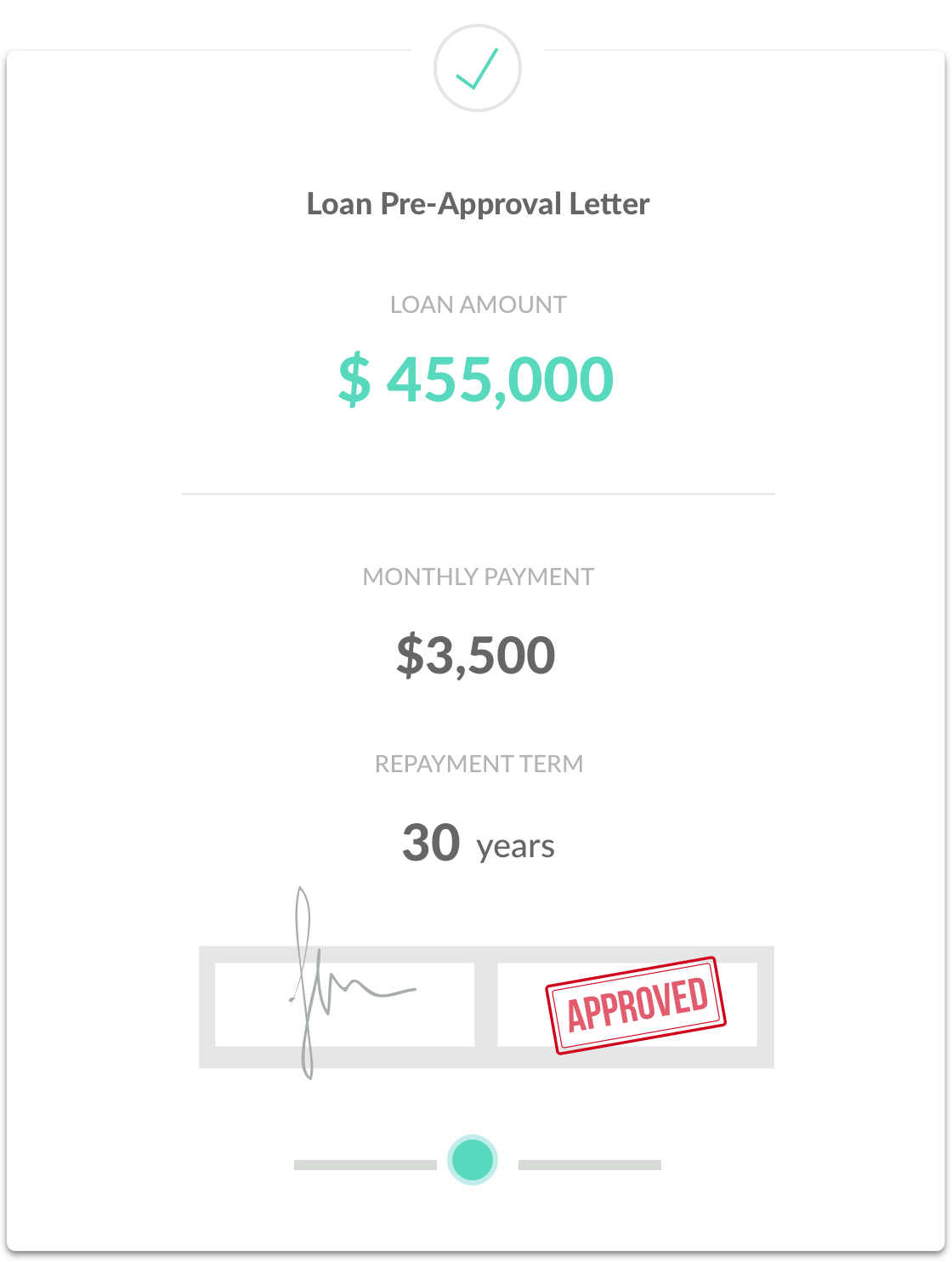

Step One:

Get pre-approval

Before you start looking for a home to buy, it’s wise and proactive to meet with a lender to get pre-approved for a loan amount. Offers accompanied by a pre-approval letter are stronger and will stand out, especially when the seller is receiving multiple offers.

To gain pre-approval, your preferred lender will gather information about income, assets, and debts to help determine how much you can borrow. This includes gathering a credit report, W-2 forms, pay stubs, federal tax returns, and recent bank statements.

There are a variety of home loan programs offering different advantages depending on your unique needs and preferences. Your preferred lender can go over the specifics of each to ensure you find a loan option that best aligns with your needs.

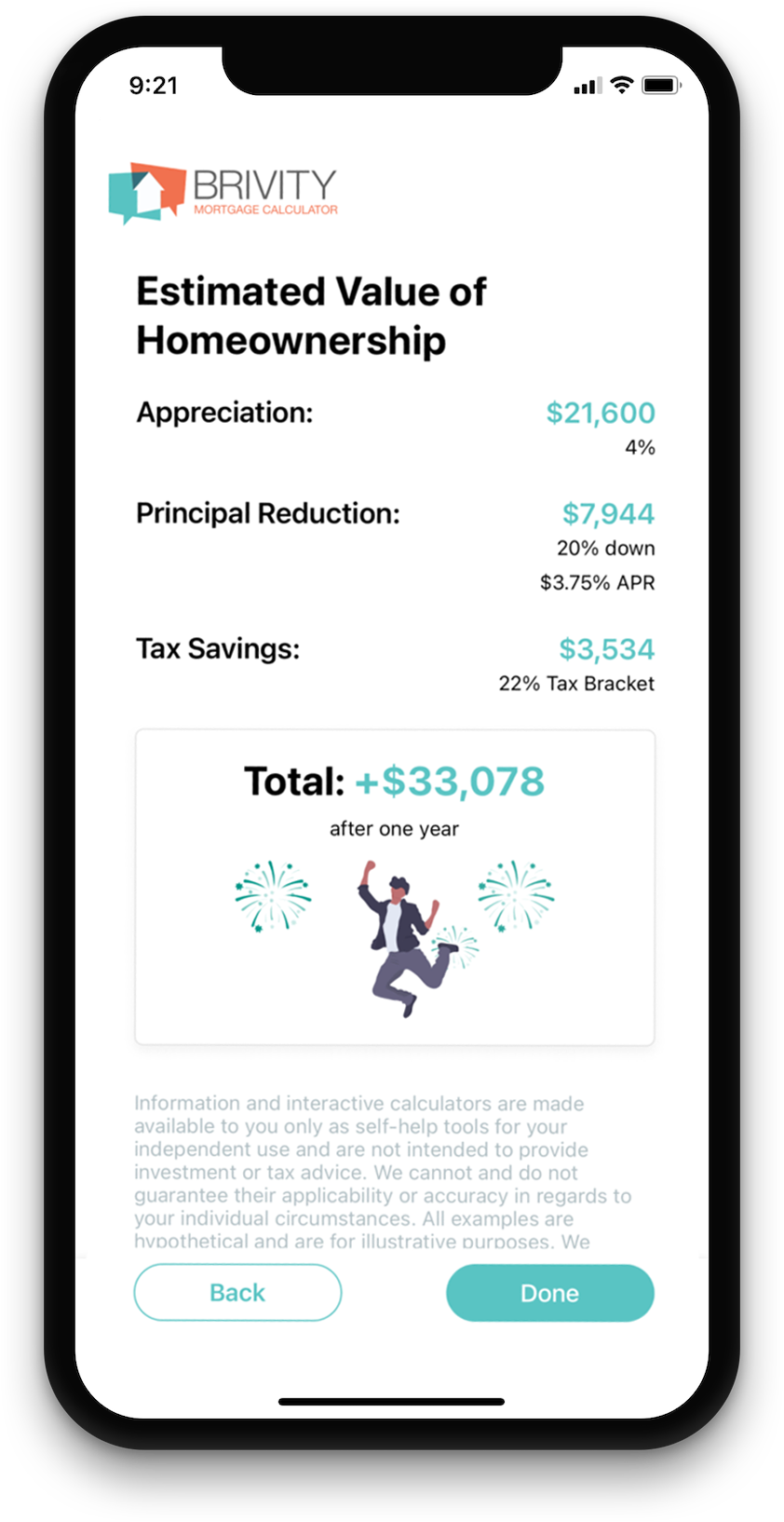

Estimate Your Monthly Payment

Estimate your mortgage payment, including the principal and interest, taxes, insurance, HOA, and Private Mortgage Insurance.

Price

Annual Tax

Loan Term (Years)

Down Payment %

Interest Rate %

Monthly HOA

Monthly Insurance

$3,198.20

Estimated Monthly Payment

Principal

$2,398.20

(75.0%)Taxes

$500.00

(15.6%)HOA

$100.00

(3.1%)Insurance

$200.00

(6.3%)Step Two:

Find the best loan

Collaborating with a top-notch local loan officer will ensure you have access to competitive rates and programs that best fit your individual needs. Take the first step by completing this form to get connected today!

Step Three:

Application and Processing

When you find the perfect property and your offer is accepted, your lender will help you complete a full mortgage loan application, discuss down payment options, and explain any related fees.

Then, your application is submitted for processing where the documents are reviewed. Your lender will also order a home appraisal and a property title search.

The next part of the application process involves sending everything to an underwriter who will review and approve the entire loan package to make sure it meets all compliance regulations.

It is not unusual to receive requests for additional documentation or clarification during this phase of the application process.

Step Four:

Signing and Finalizing the deal

Once your loan is approved, you’ll need to set up homeowners insurance.

Your documents will be sent to the title company and the closing will be scheduled for you to sign the necessary paperwork and pay any additional costs to complete the purchase of your new home.

After the loan goes through the required recording process, the purchase is complete, and you officially own your new home!